The Illicit Market for Credit Card Data

The illicit market for credit card data thrives in the hidden corners of the internet, operating as a sophisticated digital black market. Fueled by data breaches and phishing scams, these underground forums are where stolen information is packaged and sold to the highest bidder. Access to these bazaars of fraud is often gated through specialized credit card dark web links, which lead to storefronts on networks like Tor. On these platforms, vendors with reputations to uphold offer dumps of card details, complete with CVV numbers and personal identification information. A prospective buyer might use a specific gateway, such as a link to http://abacusborncrffug2ytuqx3fczqbou4mrev56pfliv7ipjfi4uib7cad.onion, to enter a marketplace where the tools for financial crime are readily available for purchase, perpetuating a global cycle of theft and fraud.

How Stolen Card Information is Sold

The illicit market for credit card data operates as a sophisticated digital black market, primarily hidden within the unindexed corners of the internet known as the dark web. Here, vast quantities of stolen card information are systematically categorized and sold to fraudsters. This information, often referred to as “dumps” for the magnetic stripe data and “fullz” for complete identity profiles, is typically obtained through large-scale data breaches, skimming devices, or phishing campaigns. The entire ecosystem thrives on anonymity and cryptocurrency transactions, creating a persistent challenge for global financial security.

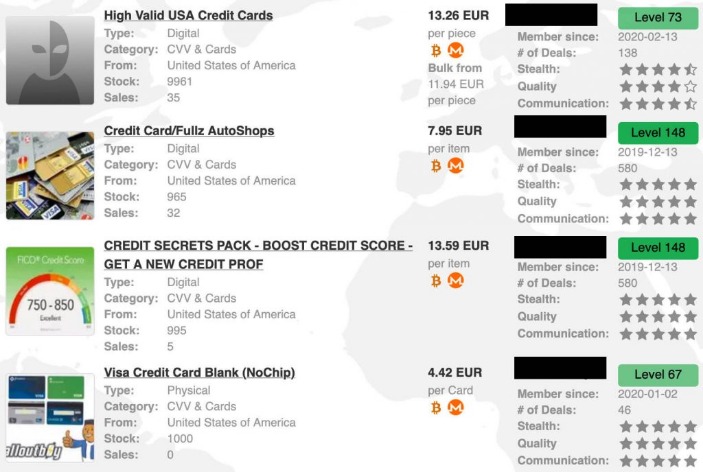

The sale of this stolen information is highly organized. Vendors on these platforms offer a range of products, from single card details to bulk packages containing thousands of records. Prices vary based on the card’s type, issuing bank, country of origin, and the freshness of the data, with recently stolen information commanding a premium. To establish trust and credibility in an environment rife with deception, sellers rely on ratings and feedback systems, much like those on legitimate e-commerce sites. This professionalization of crime lowers the barrier to entry for aspiring cybercriminals.

Access to these marketplaces and the knowledge required to exploit stolen data is often facilitated through specialized carding forums. These forums act as both educational hubs and central marketplaces where individuals can purchase stolen information, learn fraud techniques, and acquire the necessary tools. On these platforms, one can find guides on how to use the stolen data for making fraudulent online purchases or for creating cloned physical cards. The community aspect of these forums provides a support network for criminals, fostering collaboration and the continuous evolution of fraud tactics.

For financial institutions and consumers, the existence of this robust underground economy underscores the critical importance of proactive security measures. Continuous transaction monitoring for unusual activity, the widespread adoption of EMV chip technology, and the use of multi-factor authentication are essential defenses. The illicit market for credit card data is not a minor nuisance but a well-established, global criminal enterprise that adapts quickly to countermeasures, making constant vigilance and advanced cybersecurity practices non-negotiable in the fight against financial fraud.

Pricing and Factors Affecting Value

The illicit market for credit card data operates as a sophisticated, globalized economy on hidden corners of the internet. Potential buyers can browse through vast digital storefronts where vendors offer “dumps” (data from the card’s magnetic stripe) and “CVV2” (card number, expiration date, and CVV code) in bulk or as single items. The pricing for this stolen information is not arbitrary; it is a direct reflection of the perceived potential for financial gain and the costs associated with the fraud.

Several key factors determine the value of a credit card record on these platforms. The card’s issuing country and bank are primary considerations, with cards from the United States generally commanding the highest prices due to higher credit limits and less stringent fraud detection systems compared to many other regions. The type of card is also critical, as platinum, business, and corporate cards are valued significantly higher than standard debit or classic credit cards because of their elevated spending ceilings.

The freshness of the data is paramount. A “fresh” card, meaning one that was recently stolen and has not yet been reported as compromised, is far more valuable than older stock. Vendors who can consistently provide newly-acquired data can build a strong reputation and charge premium prices. Furthermore, the completeness of the data package influences cost; a simple CVV number sells for less than a “fullz,” which includes the cardholder’s full name, address, and sometimes even social security number, enabling more extensive identity theft.

Within the hidden forums and marketplaces that facilitate this trade, trust and reputation are the bedrock of all transactions. These carder communities rely on vendor rating systems and escrow services to mitigate the inherent risks of trading in an illegal environment. A vendor with a long history of providing “good” or high-valid data can charge more, as buyers are willing to pay a premium to avoid being scammed with invalid or already-canceled card information. This self-policing ecosystem ensures that pricing remains dynamic, responding to the principles of supply, demand, and perceived risk.

Marketplace Structure and Operations

The illicit market for credit card data is a sophisticated and sprawling digital economy operating primarily within the hidden corners of the internet. Fueled by constant data breaches, phishing campaigns, and malware attacks, this underground network thrives on the theft and resale of financial information. The operational core of this trade occurs on specialized black market sites, which function similarly to legitimate e-commerce platforms but are designed to facilitate anonymous criminal transactions.

The structure of these marketplaces is highly organized, featuring a clear division of labor among various actors. Vendors offer stolen data, administrators manage the platform and resolve disputes, and buyers range from individual fraudsters to organized criminal groups. Trust and reputation are paramount, with many sites implementing elaborate feedback and escrow systems to ensure the quality of the data being sold and to protect both buyers and sellers from scams.

The types of credit card data available for purchase are diverse and categorized to meet specific fraudulent needs. Common listings include:

- CVV2 Dumps: Basic card information including the card number, expiration date, and CVV code, primarily used for online card-not-present transactions.

- Fullz: Comprehensive packages that include the credit card details along with the cardholder’s full name, address, Social Security number, and date of birth, enabling identity theft and account takeovers.

- Dumps: Data extracted from the magnetic stripe of a physical card, which can be encoded onto a blank card to create a counterfeit clone for use in ATMs or point-of-sale terminals.

The operations on these black market sites are characterized by their efficiency and global reach. Transactions are typically conducted using cryptocurrencies to maintain anonymity and avoid traditional financial oversight. The entire ecosystem is resilient, with forums and communication channels existing separately from the main marketplaces to facilitate recruitment, technical support, and the promotion of new black market sites when old ones are taken down by law enforcement.

How Credit Card Data is Stolen

Credit card data is stolen through a variety of methods, from sophisticated digital skimming on e-commerce sites to the physical theft of card information. Once obtained, this stolen financial information is compiled into large databases and sold to other criminals. These illicit marketplaces are often hidden on the dark web, where vendors and buyers operate with anonymity. A thriving underground economy exists on these platforms, with credit card dark web links providing direct access to shops selling everything from single card details to bulk dumps. For instance, a marketplace like the one found at Abacus Market exemplifies the kind of hidden service where such illegal transactions occur. The availability of these credit card dark web links makes it easy for fraudsters to acquire the tools needed for financial crime, perpetuating a cycle of theft and loss.

Common Methods: Data Breaches and Phishing

Credit card details found on the dark web often originate from large-scale theft in the digital world. The journey from a legitimate transaction to a dark web listing typically begins with one of several common attack vectors.

One of the most significant sources of stolen payment information is a data breach. In these incidents, cybercriminals infiltrate the systems of retailers, payment processors, or online service providers. They exploit security vulnerabilities to access databases containing millions of customer records, including names, addresses, and credit card numbers. This stolen information is then compiled into large datasets and sold to other criminals on dark web marketplaces. The scale of a single data breach can fuel the dark web economy for months.

Another prevalent method is phishing. In these schemes, criminals send deceptive emails or text messages designed to appear as if they are from a trusted source, such as a bank or a popular online store. The messages create a sense of urgency, prompting the victim to click a link that leads to a fraudulent website. Once there, the victim is tricked into entering their credit card details and other personal information, which is immediately harvested by the attacker. This directly captured data is highly valuable and quickly finds its way to dark web vendors.

The Role of Skimming Devices

While many consumers fear sophisticated digital attacks, a significant portion of the credit card data sold on dark web links originates from a decidedly low-tech source: skimming devices. These malicious tools are physically installed on legitimate payment terminals, such as gas pumps or ATMs, to clandestinely capture the data from a card’s magnetic stripe. When a customer swipes their card, the skimmer reads and stores all the information contained on the stripe, while a hidden camera or an overlay on the keypad records the PIN. This stolen data is then encoded onto blank cards, creating clones used for unauthorized purchases and cash withdrawals, fueling a cycle of payment card fraud.

The proliferation of skimming devices directly supplies the underground economy of the dark web. Once criminals have harvested a batch of card data, they compile it into easily distributable files and list them for sale on hidden marketplaces. The data is often sold in bulk, with vendors offering “fresh” cards guaranteed to have high balances. This accessibility of stolen information lowers the barrier for entry for other criminals, enabling them to purchase the data and commit fraud without ever needing to build or install a skimmer themselves. The entire ecosystem, from physical theft to digital sale, is a well-oiled machine built on the exploitation of everyday financial transactions.

Ultimately, the presence of vast quantities of card data on dark web links is a testament to the continued effectiveness of skimming. Despite the push for more secure chip technology, the reliance on the magnetic stripe for fallback transactions in many regions leaves consumers vulnerable. Each successful skim translates directly into another set of financial details available for purchase by fraudsters, highlighting the critical need for both consumer vigilance at physical terminals and the global adoption of more secure payment protocols to disrupt this pipeline of stolen information.

From Theft to Sale on the Dark Web

The journey of a stolen credit card from a legitimate transaction to a product on the illegal marketplaces is a sophisticated criminal process. It begins with data thieves employing a variety of methods to harvest card details from unsuspecting consumers and vulnerable businesses.

Thieves acquire credit card data through several primary channels. Skimming devices are placed on ATMs or gas station pumps to capture data from a card’s magnetic stripe. Data breaches target large retailers or payment processors, exposing millions of records at once. Phishing attacks trick individuals into entering their details on fake websites, while malware can log keystrokes or infiltrate point-of-sale systems to siphon information directly.

Once stolen, the raw data is compiled and prepared for sale. This involves organizing the information into a standardized format that typically includes the card number, expiration date, CVV code, and sometimes the cardholder’s name and address. This data is then bundled and advertised on hidden forums and dark web sites.

- Carding forums where vendors are rated based on the validity of their data.

- Automated shops that allow buyers to search for cards by country, bank, or credit limit.

- Private channels on encrypted messaging apps for high-volume transactions.

The final step is the sale and monetization. Buyers on these illegal marketplaces purchase the card data for a fraction of the card’s value. They then use the information to make fraudulent online purchases, create counterfeit physical cards, or resell the data again. The entire ecosystem thrives on anonymity and the constant supply of fresh, valid card details from ongoing theft operations.

Risks and Consequences

Navigating the digital underworld to find credit card dark web links is an endeavor fraught with extreme peril. The consequences extend far beyond the immediate legal jeopardy, as these marketplaces are hotbeds for sophisticated scams. Purchasing from a site like Abacus Market not only funds criminal enterprises but also exposes buyers to severe financial fraud and identity theft, turning a single search into a life-altering catastrophe.

Financial Losses for Consumers and Businesses

The trade in credit card information on the dark web represents a significant and direct threat to the financial health of both individuals and companies. When card details are stolen and sold in bulk, the primary risk is comprehensive financial fraud, leading to immediate and often severe monetary losses. For consumers, the consequences extend far beyond the initial unauthorized charges, impacting credit scores and creating a lengthy bureaucratic nightmare to resolve.

For businesses, the fallout is equally damaging. They face direct financial losses from chargebacks and the costs associated with investigating and resolving fraudulent transactions. Furthermore, a security breach that leads to customer data being sold on the dark web erodes consumer trust, damages the brand’s reputation irreparably, and can result in substantial regulatory fines for failing to protect sensitive information.

- Direct theft of funds from consumer bank accounts.

- Costly chargeback fees and lost merchandise for merchants.

- Expenses for re-issuing compromised credit cards.

- Long-term damage to credit scores for affected individuals.

- Regulatory fines and legal fees for businesses that experienced a data breach.

- Loss of customer trust and future revenue due to reputational harm.

The Impact of Chargeback Fraud

The proliferation of credit card information on the dark web creates a direct and costly threat to the global financial ecosystem, with chargeback fraud representing a significant consequence for merchants. When criminals purchase stolen card details from these underground markets, they initiate fraudulent transactions. The legitimate cardholder, upon discovering the unauthorized charge, rightfully files a dispute with their bank, triggering the chargeback process. While this consumer protection is vital, its abuse through so-called “friendly fraud” places an immense burden on businesses, who are often left liable for the lost revenue, the cost of the merchandise, and additional processing fees.

For businesses, the impact of chargeback fraud extends far beyond the immediate financial loss. Each dispute incurs non-refundable fees from payment processors, and a high chargeback ratio can lead to catastrophic penalties. Payment gateways and acquiring banks monitor this ratio closely; exceeding their strict threshold can result in a merchant’s account being terminated, effectively severing their ability to accept card payments. This operational risk is a direct consequence of criminal activity fueled by the trade in stolen data on hidden online platforms.

The cycle of fraud is intrinsically linked to the initial compromise of personal data. The availability of credit card details on the dark web is frequently the result of large-scale data breaches that expose millions of consumer records. This constant flow of new information from corporate intrusions ensures that the underground market remains stocked with fresh, valid card data, perpetuating the cycle of fraudulent transactions and subsequent chargebacks that businesses are forced to combat.

Ultimately, the entire financial chain bears the cost. While consumers are shielded from direct liability, they face the inconvenience of card replacement and heightened security monitoring. The financial institutions and payment networks invest heavily in sophisticated fraud detection systems. However, the primary financial and operational burden disproportionately falls on merchants, who must navigate the complex challenge of verifying legitimate orders while rejecting fraudulent ones, all while operating under the constant threat of punitive measures from the very systems that enable their commerce.

Global Scale of the Problem

The trade in credit card information on the dark web represents a severe and immediate threat to global financial security. For individuals, the consequences are profoundly personal, ranging from drained bank accounts and unauthorized purchases to the long and arduous process of reclaiming one’s financial identity. Victims often face damaged credit scores, rejected loan applications, and hours spent contesting fraudulent charges with banks, a process that can inflict significant emotional and financial stress long after the initial fraud occurs.

On a global scale, this illicit economy fuels a multi-billion dollar criminal enterprise that undermines the integrity of financial systems worldwide. The sheer volume of data available is staggering, with millions of card details being bought and sold at any given moment. This widespread availability is a direct result of the continuous cycle of data breaches that afflict organizations of all sizes, from major corporations to small local businesses. Each breach injects a fresh supply of information into the black market, perpetuating the cycle of fraud and enabling criminal networks to operate on an industrial scale.

- It’s also a good idea to set up a VPN for an extra layer of protection.

- Most ransomware gangs have a presence in the dark web today, where they announce their attacks.

- This is considered as one of the largest data breaches in history 5 and a serious concern for all.

- Our clients have shared positive reviews ⭐⭐⭐⭐⭐ with us about these shops, and our team has also vetted them, so they are 99% trusted.

- As with credit cards, the location of the victim whose information is up for sale has a significant influence on price.

- If you have to make a purchase immediately, create a password-protected hotspot to connect to your phone’s cellular data instead.

The risks extend beyond individual financial loss to impact the broader economic landscape. Financial institutions and merchants absorb billions in losses annually from card-not-present fraud and chargebacks, costs that are ultimately passed on to consumers through higher fees and prices. Furthermore, the existence of these markets erodes public trust in digital commerce and payment systems. The persistent threat necessitates massive global investment in cybersecurity measures, fraud detection systems, and international law enforcement cooperation, making the fight against this shadow economy a persistent and costly global challenge.

Detection and Prevention

In the digital age, the detection and prevention of financial fraud are paramount for safeguarding assets. A significant threat emerges from the trade of stolen payment information on hidden online markets, where criminals actively sell credit card dark web links to the highest bidder. Proactive monitoring for these data breaches, alongside robust security protocols, is essential to prevent unauthorized access and financial loss. For instance, a marketplace like http://aresbuy2pgeaolftrbhcxlsbg5qw35wer77h45egg4omainek2gtpxid.onion exemplifies the platforms where such illicit exchanges occur, highlighting the critical need for advanced cybersecurity measures to protect consumers from the dangers associated with exposed credit card dark web links.

Monitoring Accounts and Statements

Protecting your financial identity begins with proactive detection and prevention strategies. The illicit trade of stolen credit card data on hidden online platforms is a persistent threat, making it crucial to implement strong security measures. Prevention is your first line of defense; this includes using complex, unique passwords for all financial accounts, enabling multi-factor authentication wherever possible, and being extremely cautious about where you enter your card details online. Never respond to unsolicited requests for your information via phone, email, or text.

Vigilant monitoring of your accounts and statements is an equally critical component of your financial security. You should make a habit of reviewing your transaction history frequently through your bank’s mobile app or online portal, not just waiting for the monthly statement. Scrutinize every charge, no matter how small, as criminals often test cards with minor transactions first. Set up real-time alerts for purchases, cash advances, and international transactions to be notified of activity instantly. This constant oversight allows you to identify and report fraudulent charges immediately, significantly limiting the damage and facilitating a quicker resolution from your card issuer.

Combining these robust prevention techniques with diligent monitoring creates a powerful shield against financial fraud. By taking these steps, you are not only safeguarding your current assets but also protecting your credit score and long-term financial health from the repercussions of identity theft. A proactive and consistent approach is the most effective way to ensure your financial information remains secure in an increasingly digital world.

Utilizing Fraud Alerts and Tracking Tools

Protecting your financial information begins with proactive detection and prevention strategies. The moment a credit card is identified as being at risk, immediate action is required to mitigate potential damage. This involves a multi-layered approach that combines personal vigilance with institutional security measures to create a formidable defense against unauthorized use.

A powerful first line of defense is the utilization of fraud alerts. Placing a fraud alert on your credit file with the major bureaus requires creditors to take extra steps to verify your identity before issuing new credit in your name. This can effectively stop an identity thief from opening new accounts even if they possess your personal details. For more comprehensive protection, a credit freeze is the most robust option, completely locking access to your credit report, thus preventing new accounts from being opened altogether.

Complementing these alerts, continuous monitoring through tracking tools is essential. Many financial institutions and credit monitoring services offer real-time alerts for suspicious transactions. These systems scan for unusual activity, such as purchases in distant locations or for atypical amounts, providing an early warning system. This constant digital surveillance is crucial because stolen card information is often quickly sold on illegal marketplaces, making rapid detection paramount.

Ultimately, a proactive stance is your greatest asset. Regularly reviewing your bank and credit card statements for any discrepancies, no matter how small, can uncover fraudulent activity early. By combining the official barriers of fraud alerts with the constant oversight of tracking tools, you create a resilient security framework that protects your assets from the moment they appear in the shadows of the digital underworld.

Strong Security Practices for Protection

Credit card dark web links are a primary vector for the sale of stolen financial data, posing a severe threat to individuals and financial institutions alike. These links, often shared within hidden forums and marketplaces, provide direct access to illicit bazaars where card details are traded as commodities. The data sold typically includes the cardholder’s name, the credit card number, expiration date, and the CVV code, often bundled with other personal information to fetch a higher price. This ecosystem thrives on the anonymity provided by specialized networks, making it a persistent challenge for law enforcement and cybersecurity professionals.

Detection of such compromised information requires proactive and continuous monitoring. Organizations and individuals can utilize dark web monitoring services that scan these hidden corners of the internet for specific data points, such as card numbers or email addresses. When a match is found, it serves as an early warning that an account has been breached. For financial institutions, advanced fraud detection systems that analyze transaction patterns in real-time are critical. These systems employ machine learning to flag anomalies, such as a sudden spike in online purchases or transactions originating from a geographic location inconsistent with the cardholder’s history, enabling immediate intervention.

Prevention is fundamentally rooted in the adoption of strong security practices. For consumers, this means enabling multi-factor authentication on all financial and email accounts, using unique and complex passwords for each service, and reviewing bank statements regularly for any unauthorized activity. It is also crucial to be wary of phishing attempts, which are a common method used to harvest card details. For businesses, protecting customer data is a paramount responsibility. This involves implementing robust encryption for data both in transit and at rest, adhering to the PCI DSS compliance standards, and conducting regular security audits and employee training to mitigate human error.

The underground economy supporting this trade is sustained by carder communities, where individuals share techniques, tools, and stolen data. Engaging in or accessing these groups is not only illegal but extremely dangerous. Therefore, the most effective protection is a layered security approach that combines technological solutions with vigilant personal habits. By understanding the methods used by criminals and proactively securing personal information, the risk of falling victim to this type of fraud can be significantly reduced.

Technological Defenses and Future Trends

As the illicit trade of stolen financial data thrives, technological defenses are the primary bulwark against the sale of credit card dark web links. Financial institutions and cybersecurity firms are deploying advanced artificial intelligence to monitor for data breaches in real-time, while the proliferation of tokenization renders stolen card numbers useless to criminals. Future trends point towards a more integrated security posture, where behavioral biometrics and decentralized identity systems will create unprecedented hurdles for fraudsters attempting to profit from these compromised credentials. The ongoing battle is exemplified by the constant takedown of marketplaces operating on hidden services, such as those previously accessible at nexusafejew45osqaawl2xqjwmincsfvjwuwtm2fums2kjeon7tbmlid, highlighting the persistent challenge.

AI and Advanced Fraud Detection Systems

The proliferation of credit card data on the dark web represents a persistent and evolving threat to global financial security. In response, the technological defenses employed by financial institutions and cybersecurity firms have grown increasingly sophisticated, moving beyond simple rule-based alerts to complex, intelligent systems capable of predictive analysis. The primary goal is to shift from a reactive to a proactive posture, identifying and neutralizing threats before they can be monetized by criminals operating on underground platforms, including the various CVV shops that specialize in the sale of this stolen data.

Current and emerging technologies are fundamentally changing the fraud detection landscape. These systems analyze vast datasets in real-time, looking for subtle anomalies that would be invisible to human reviewers. Key technological defenses and future trends include:

- Machine Learning and Behavioral Analytics: AI models are trained on historical transaction data to establish a baseline of normal behavior for each cardholder. They can then flag transactions that deviate from this pattern, such as an unusual purchase location or time of day, with a high degree of accuracy.

- Network Graph Analysis: This technique maps the relationships between different entities—such as cards, merchants, IP addresses, and devices—to identify organized fraud rings. If multiple cards reported as stolen are used from the same device or IP cluster, the system can preemptively block other cards associated with that network.

- Biometric Authentication: The integration of fingerprint, facial, and voice recognition adds a powerful layer of security that is extremely difficult for fraudsters to replicate, moving validation from something the user has (a card number) to something the user is.

- Real-Time Consortium Data: Financial institutions are increasingly participating in data consortia, sharing anonymized information about fraudulent activities and compromised cards in real-time. This creates a collective immune system, allowing one bank’s discovery of a breach to instantly protect customers at all other member banks.

The future of combating credit card fraud on the dark web lies in the continued advancement of AI. Next-generation systems will leverage deep learning to understand the temporal and contextual nuances of fraud campaigns, potentially predicting the emergence of new CVV shops based on chatter and data flow patterns. The integration of these advanced systems creates a dynamic and adaptive defense, making it significantly more challenging for criminals to profit from stolen payment card information.

E-commerce Risks and Security Measures

The trade in credit card dark web links represents a persistent and highly organized cybercrime ecosystem. These links, often harvested through sophisticated methods, provide direct access to compromised payment card data, fueling fraudulent transactions and identity theft. The very existence of this marketplace is a direct consequence of data breaches at retailers, financial institutions, and online service providers, where vast databases of customer information are exfiltrated and later monetized in these hidden corners of the internet.

To combat this threat, e-commerce platforms and financial entities deploy a multi-layered technological defense strategy. These measures are designed to prevent the initial theft of data and to render stolen information useless.

- Tokenization: This technology replaces sensitive card details with a unique, randomly generated token. Even if a data breach occurs, the stolen tokens are worthless outside of the specific transaction context for which they were created.

- End-to-End Encryption (E2EE): Data is encrypted at the point of entry, such as a payment terminal, and remains encrypted throughout its journey to the processor. This ensures that card information is never exposed in plain text within a merchant’s system.

- Multi-Factor Authentication (MFA): By requiring a second form of verification beyond a password, MFA significantly raises the barrier for unauthorized account access, protecting stored card details on user accounts.

- Advanced Fraud Detection Systems: Powered by artificial intelligence and machine learning, these systems analyze transaction patterns in real-time to flag anomalies, such as purchases from unfamiliar locations or unusual spending amounts.

Looking forward, the landscape of credit card security is evolving rapidly. Future trends point towards a passwordless and more integrated authentication experience. Biometric verification, including fingerprint and facial recognition, is becoming a standard feature for authorizing payments. Furthermore, the adoption of EMV 3-D Secure (3DS2) protocol provides a more seamless yet secure checkout flow by enabling richer data exchange between merchants, card issuers, and payment networks for risk analysis. The continued expansion of real-time payment networks also introduces new paradigms for instant, account-to-account transfers that can potentially bypass the traditional card infrastructure altogether, thereby reducing the attack surface for card data theft.

The Role of Encryption and Multi-Factor Authentication

In the ongoing battle against credit card fraud, technological defenses form the primary barrier between consumer data and criminals. The core of this defense lies in robust encryption and multi-factor authentication (MFA). Encryption acts as the first and most critical line of protection, scrambling sensitive information such as credit card numbers during transmission and while at rest, rendering it useless to any unauthorized party who intercepts it. Without the specific decryption key, the stolen data remains an indecipherable string of characters, significantly devaluing it on illegal marketplaces.

Complementing encryption, multi-factor authentication adds a powerful, dynamic layer of security that moves beyond static passwords. By requiring a second or third form of verification—such as a biometric scan, a hardware token, or a one-time code sent to a mobile device—MFA ensures that even if login credentials or a primary account number are stolen, they are insufficient to complete a fraudulent transaction or access an account. This drastically reduces the risk of account takeover and unauthorized use, protecting both the financial institution and the cardholder from the consequences of data breaches.

Looking toward future trends, the evolution of these technologies is continuous and necessary. The adoption of post-quantum cryptography is being prioritized to develop encryption algorithms that can withstand attacks from future quantum computers, which threaten to break current cryptographic standards. Furthermore, the move toward passwordless authentication, leveraging biometrics and FIDO2 standards, promises a more seamless yet secure user experience. These advancements, combined with AI-driven behavioral analytics that can detect anomalous spending patterns in real-time, are shaping a security landscape where defenses are not only stronger but also more adaptive and intelligent, staying one step ahead of the threats lurking in the digital shadows.