The Dark Web Environment

- Now that we understand why individuals are enticed to buy credit cards on the Dark Web, let us explore the risks and challenges involved in these transactions and how to navigate this treacherous landscape.

- Increased international cooperation between law enforcement agencies will become essential, targeting global criminal networks through coordinated actions and intelligence sharing.

- It maintains a very strict level of user verification and integration with an official Telegram account to provide real-time updates to users.

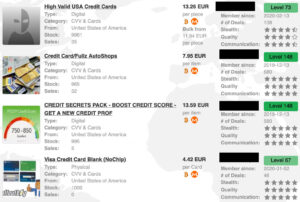

The dark web provides a clandestine digital marketplace where illicit goods and services are traded with a high degree of anonymity. Among the most prevalent and damaging commodities available in this shadowy economy are stolen financial details. For a price, individuals can engage in buying credit cards on the dark web, acquiring card numbers, expiration dates, and CVV codes siphoned from unsuspecting victims. This activity fuels a multi-billion dollar cycle of fraud, with vendors operating on specialized platforms. For instance, some users may find their way to a resource like the Abacus Market to browse these illegal offerings. The entire process of buying credit cards on the dark web is facilitated by cryptocurrencies and encrypted communication, creating a persistent challenge for global cybersecurity efforts.

Definition and Anonymity

The dark web is a deliberately concealed segment of the internet, inaccessible through standard browsers like Chrome or Firefox. It requires specialized software, such as Tor, which routes traffic through multiple layers of encryption to obscure a user’s location and usage. This environment is designed to provide a high degree of anonymity, making it a haven for both privacy-conscious individuals and illicit activities. The core principle is the separation of a user’s identity from their online actions, a feature that, while valuable for dissidents and journalists, also facilitates illegal marketplaces.

Within this hidden ecosystem, a thriving black market exists for stolen financial data. Among the most common goods for sale are credit card details, which are packaged and sold in bulk. These marketplaces, often referred to as CVV shops, operate as digital storefronts where criminals can purchase card information that has been skimmed, phished, or hacked from vulnerable databases. The entire process, from browsing to transaction, is designed to leverage the dark web’s anonymity.

- Credit card “dumps” (data from the card’s magnetic stripe).

- CVV2 numbers (the three-digit code on the back of the card).

- Fullz (complete personal information including name, address, and Social Security Number).

- Bank account login credentials.

The allure for buyers is the potential for significant financial gain through fraud, while sellers profit from monetizing stolen data. The anonymous nature of the dark web and the use of cryptocurrencies make these transactions difficult to trace. However, engaging with a CVV shops is a serious criminal offense, and law enforcement agencies globally actively monitor these spaces. Furthermore, these markets are rife with scams, where buyers may receive invalid data or themselves become targets. The environment is one of pervasive risk and illegality.

Access and Hidden Marketplaces

The dark web, a deliberately concealed segment of the internet accessible only through specialized software, hosts a significant underground economy. Among its most notorious offerings is the sale of stolen financial data, with credit card information being a primary commodity. This illicit marketplace thrives on anonymity, creating a persistent challenge for global law enforcement and financial institutions.

Accessing these hidden marketplaces requires specific tools and knowledge. The most common gateway is the Tor browser, which routes internet traffic through a distributed network of relays, obscuring a user’s location and activity. Upon reaching a marketplace, a user is typically presented with a modern-looking e-commerce interface, complete with vendor ratings, customer reviews, and shopping carts, all operating in the shadows. The entire ecosystem, from the theft of data to its final sale, is often referred to as carding.

The process of buying credit cards on these platforms is disturbingly straightforward. Listings, often called “dumps,” provide detailed information including the card number, expiration date, CVV code, and sometimes the cardholder’s name and address. Prices vary based on the card’s type, issuing bank, credit limit, and the freshness of the data. Purchases are almost exclusively made with cryptocurrencies to maintain transactional anonymity.

Engaging in this activity carries severe consequences. Buyers risk significant financial loss through scams, as there is no recourse for faulty goods. More importantly, participation in carding is a serious criminal offense, leading to prosecution, imprisonment, and a permanent criminal record. The entire environment is built on exploitation and theft, causing tangible harm to individuals and businesses worldwide.

Distinction from Legitimate Uses

The dark web, a deliberately concealed segment of the internet accessible only through specialized software, hosts a thriving and illicit marketplace for financial data, with the sale of stolen credit cards being a primary commodity. This environment operates with a degree of anonymity that shields both vendors and buyers from conventional law enforcement scrutiny, creating a persistent challenge for global financial security. The cards, often obtained through large-scale data breaches or phishing campaigns, are sold in bulk or individually, with prices varying based on the card’s type, issuing bank, perceived credit limit, and the freshness of the data.

It is crucial to distinguish this criminal activity from the legitimate uses of anonymity-focused networks. The same technology that powers these black markets also provides a secure communication channel for journalists, whistleblowers, and political dissidents operating under oppressive regimes. Law enforcement agencies themselves utilize the dark web for covert operations and intelligence gathering. The distinction lies not in the tool but in its application; the dark web is a double-edged sword, capable of protecting both free speech and criminal enterprise.

Within these illicit marketplaces, a buyer’s perceived safety often hinges on the vendor reputation, which is meticulously built through transaction histories and user feedback on the marketplace forums. A vendor with a long-standing and positive vendor reputation is more likely to provide valid, high-quality card data, as their financial success depends on maintaining trust within this lawless ecosystem. Despite this internal mechanism of trust, any engagement in purchasing these cards is a serious felony, supporting a global criminal network that victimizes individuals and financial institutions alike.

Motivations for Purchase

Understanding the motivations for purchasing illicit goods is key to comprehending the digital underground economy. When it comes to buying credit cards on the dark web, the primary drivers are often a combination of perceived anonymity, financial desperation, and the allure of easy gains. Individuals are drawn to these markets, such as Abacus Market, by the promise of quick financial solutions, ignoring the significant legal and ethical consequences. The entire ecosystem of buying credit cards on the dark web thrives on exploiting these vulnerabilities for profit.

Profit Potential and Low Cost

For a specific type of criminal, the dark web serves as a one-stop marketplace for illicit financial gain, with stolen credit card data being a primary commodity. The motivations for these purchases are straightforward and driven by immediate financial opportunity. Individuals seek to acquire card details not for personal use in a traditional sense, but to monetize them quickly through fraudulent purchases or by reselling the information to other criminals. The appeal lies in the direct access to financial instruments that can be liquidated for cash or high-value goods with minimal initial investment.

The profit potential from this activity is significant, acting as the primary engine for the entire ecosystem. Once a fraudster obtains a set of card numbers, they can exploit the available credit line to its maximum. This often involves purchasing easily resellable items like electronics, gift cards, or luxury goods before the card is reported stolen and canceled. The entire process is a race against time, but the returns can be substantial for those who move quickly. The quality of the data is paramount, and listings often boast of fresh dumps track 1&2 which contain the embedded magnetic stripe information needed to clone physical cards, thereby unlocking higher value.

This criminal pursuit is further incentivized by its remarkably low cost of entry. The price for a single credit card’s information, including the crucial track data, is often shockingly low compared to the potential credit limit it represents. This low barrier allows aspiring fraudsters to start with minimal capital, scaling their operations as they profit. The combination of high reward and low risk from a cost perspective creates a perceived opportunity that continues to fuel this illegal market, despite the severe legal consequences involved.

Anonymity for Buyers and Sellers

Motivations for purchasing credit card information on the dark web are diverse and often financially driven. Buyers, typically cybercriminals, seek this data to commit fraud, such as making unauthorized purchases, withdrawing cash, or creating cloned physical cards. The low cost of bulk card data compared to the potential high value of the stolen funds makes this a high-reward, low-risk endeavor from the criminal’s perspective. The primary goal is to monetize the stolen information quickly and efficiently before the card is reported as compromised.

Anonymity is the cornerstone of these illicit transactions, serving as a critical shield for both buyers and sellers. The dark web’s infrastructure, accessed through specialized software, obscures user identities and locations. Buyers can operate without revealing their real-world identities, mitigating the immediate risk of legal repercussions. For sellers, this anonymity is equally vital, allowing them to operate illegal marketplaces and build a client base while evading law enforcement. The perceived safety of this hidden ecosystem is what fuels the entire underground economy.

Within this anonymous marketplace, a key factor for a successful, albeit illegal, transaction is the establishment of vendor reputation. Since no traditional legal protections exist, buyers rely heavily on feedback systems and reviews from previous customers. A seller with a consistent history of providing valid, high-balance card data will command higher prices and attract more business. This system of trust, built entirely on criminal peer review, is essential for maintaining the flow of commerce on these platforms.

Accessibility and Ease of Use

The motivations for purchasing credit cards on the dark web are primarily financial and rooted in anonymity. Buyers are often driven by the prospect of immediate, illicit gain with a perceived low risk of direct confrontation. The appeal lies in acquiring financial instruments that can be used for fraudulent purchases, cash-outs, or resale, all under the cloak of the dark web’s encryption. For these individuals, the marketplace offers a direct path to assets that would be otherwise inaccessible through legitimate means.

Accessibility is a cornerstone of these illicit markets. The dark web itself is easily reachable with standard software, and the platforms for carding are often designed with a user-friendly interface that mimics legitimate e-commerce sites. Vendors establish reputations through feedback systems, creating an environment where buyers can shop with a degree of confidence in the quality of the stolen data. This normalization of the illegal transaction process significantly lowers the barrier to entry for aspiring cybercriminals.

Finally, the ease of use extends beyond the purchasing process to the application of the stolen data. Comprehensive guides and tutorials are frequently available within these communities, detailing every step from the initial acquisition to the monetization of the cards. The entire ecosystem is built to streamline the process, making it a turnkey operation for fraud. This combination of strong motivation, high accessibility, and simple operation makes the dark web a persistent and challenging threat to financial security worldwide.

Risks and Challenges

The digital underworld presents a perilous landscape for those considering buying credit cards on the dark web. This illicit activity is fraught with significant risks, from the high probability of financial loss through scams to the severe legal repercussions of engaging in cybercrime. Even a successful transaction, such as one from a marketplace like Abacus Market, offers no guarantee of receiving functional data, leaving purchasers vulnerable and exposed. The entire process of buying credit cards on the dark web is a gamble where the stakes are one’s financial security and personal freedom.

Fraudulent Sellers and Scams

The act of purchasing credit cards on the dark web is fraught with significant risks and challenges that extend far beyond the initial illegal transaction. Buyers operate in a completely unregulated and anonymous environment where there are no guarantees, refunds, or consumer protections. The fundamental challenge is the inherent asymmetry of information; sellers can make bold claims about the validity, balance, and freshness of the card data with zero accountability. A buyer has no reliable way to verify this information until after the payment, typically in cryptocurrency, has been sent and is irrecoverable.

Navigating the marketplace itself is a primary hazard, as it is populated by fraudulent sellers and scams designed to exploit newcomers. Common schemes include “exit scams,” where a vendor with a seemingly good reputation accumulates orders and then disappears with all the funds without delivering any products. Other sellers may deliver outdated or already canceled card information, or “dumps” that have been bled dry. Some may even send malware-infected files instead of the promised data, further compromising the buyer’s own system and personal information.

Engaging in these transactions is a direct enabler of a vast criminal ecosystem built upon financial fraud. The credit card details being sold are almost always stolen from innocent individuals and businesses through data breaches, phishing attacks, or skimming devices. By funding these illicit marketplaces, buyers perpetuate the cycle of victimization and incentivize further criminal activity. The financial losses from this type of fraud are ultimately absorbed by financial institutions, merchants, and consumers through higher fees and costs.

Beyond the immediate scam, participants face severe legal consequences. Law enforcement agencies actively monitor these dark web marketplaces. An attempt to buy stolen credit card information can lead to serious charges including computer fraud, identity theft, conspiracy, and wire fraud. The perception of anonymity on the dark web is often a dangerous illusion; sophisticated tracking and investigative techniques can and do unmask users, resulting in arrest and prosecution.

Law Enforcement Operations

Law enforcement operations targeting the illicit trade of credit cards on the dark web face a complex and evolving set of risks and challenges. The fundamental obstacle is the anonymized architecture of the dark web itself, which provides a shielded marketplace for vendors and buyers to operate with perceived impunity. Identifying and locating individuals behind these anonymous profiles requires sophisticated technical capabilities, significant resources, and international cooperation, as servers and actors are often distributed across multiple jurisdictions with conflicting laws.

The sheer volume of data for sale is another significant hurdle. Stolen card information is often sold in bulk batches containing millions of records, making it difficult for authorities to prioritize interventions and provide timely notifications to all potential victims. Furthermore, the criminal ecosystem is highly adaptable; when one marketplace is taken down by police action, several others often emerge to take its place, demonstrating a resilient and hydra-like nature. This constant cat-and-mouse game strains the resources of even the most well-funded agencies.

A critical risk associated with this trade is the direct link to other forms of financial crime. Purchased card data is frequently used to create counterfeit physical cards through a process known as card cloning. This technique allows criminals to withdraw cash from ATMs or make in-person purchases, directly monetizing the stolen digital information. This physical manifestation of a digital theft blurs the lines between cyber and traditional crime units, necessitating seamless inter-agency collaboration to effectively investigate the entire chain of criminal activity, from the initial data breach to the final cash-out operation.

Cybersecurity Threats

The act of purchasing credit cards on the dark web is fraught with significant risks and challenges that extend far beyond the initial illicit transaction. Buyers operate in a completely unregulated and anonymous environment where trust is nonexistent. There is a high probability of being defrauded by sellers who provide expired, canceled, or otherwise invalid card data after payment is received. The entire process is a gamble, with the buyer having no recourse for refunds or complaints, making financial loss an almost certain initial outcome.

From a cybersecurity perspective, the threats are severe and multifaceted. Engaging in such activities exposes an individual to a high risk of malware infection. Files or links provided by sellers can be laced with trojans, keyloggers, or ransomware designed to compromise the buyer’s own system. This can lead to the theft of personal data, financial information, and even take control of the device. Furthermore, law enforcement agencies actively monitor these marketplaces, making buyers a direct target for investigation and prosecution for charges related to fraud, identity theft, and computer crimes.

The technical execution of using stolen card information presents its own set of formidable challenges. Modern financial institutions employ sophisticated fraud detection systems that analyze spending patterns, geographic location, and transaction velocity. Any anomalous activity, such as a sudden purchase in a different state or country, can trigger an immediate card cloning alert and result in the card being frozen. This renders the stolen data useless and can directly lead back to the individual attempting the fraudulent transaction, especially if they are using it for in-person purchases with a cloned physical card.

Ultimately, the entire ecosystem is designed to exploit everyone involved. While the primary victims are the original cardholders, the buyers themselves are secondary targets for scams, cyberattacks, and legal consequences. The perceived anonymity of the dark web is a fragile illusion, and the potential for severe financial and legal repercussions far outweighs any temporary gain from the fraudulent use of stolen payment credentials.

Poor Quality of Data

The most immediate risk associated with purchasing credit cards from dark web markets is the fundamental unreliability of the data being sold. Vendors operate with near-total anonymity, facing no accountability for the products they list. A listing promising a “fresh” credit card with a high balance may, in reality, be a complete fabrication, contain expired information, or offer details that have already been reported stolen and canceled by the financial institution. Buyers have no recourse for refunds or complaints, making every transaction a high-stakes gamble with a significant likelihood of receiving worthless data.

Beyond simple fraud, the poor quality of data directly fuels significant security threats for the individuals whose information is being traded. Inaccurate or outdated card details are often bundled with other personal identifying information. When this corrupted data is used to attempt fraudulent purchases or applications, it can trigger complex financial discrepancies and reporting errors for the victim. This chaotic trail of false information can severely damage a person’s credit history and complicate the recovery process, often acting as a precursor to full-scale identity theft.

Furthermore, the act of seeking out and engaging with these illicit markets exposes the buyer to substantial dangers. Law enforcement agencies actively monitor these platforms, and simply visiting them can attract unwanted scrutiny. More critically, these sites are rife with malware and phishing schemes designed to exploit visitors. Trusting any download link or file from a dark web vendor is an extreme risk, potentially leading to the buyer’s own computer being infected with keyloggers or ransomware, thereby compromising their own financial accounts and personal data in the process.

Legal and Ethical Consequences

Engaging in the purchase of credit cards on the dark web carries profound risks and challenges that extend far beyond the initial illicit transaction. Buyers operate in a completely unregulated and anonymous environment, making them prime targets for scams where sellers simply take the payment and provide nothing in return, or supply outdated and useless card information. The entire ecosystem is a hunting ground for law enforcement agencies worldwide, who employ advanced cyber-forensics to track and identify participants. Furthermore, the very act of accessing these marketplaces exposes one’s own system to a high risk of malware, ransomware, and hacking from other malicious actors who have no allegiance to anyone.

The legal and ethical consequences of this activity are severe and life-altering. From a legal standpoint, purchasing credit card information is a serious felony, prosecutable as wire fraud, identity theft, computer fraud, and conspiracy. Convictions can result in lengthy federal prison sentences, crippling financial fines, and a permanent criminal record that will severely limit future employment and housing opportunities. Ethically, this crime has a direct and devastating human impact on the victims whose financial security and personal credit are stolen, often causing significant emotional distress and years of financial hardship to recover.

- Financial Loss from seller scams and fraudulent transactions.

- Legal Prosecution for charges including identity theft and fraud.

- Malware Infection from compromised software and links.

- Personal Data Compromise leading to further identity theft.

- Severe damage to the victim’s credit and financial stability.

The data sold often includes the complete dumps track 1&2, which contains all the information encoded on the card’s magnetic stripe, allowing criminals to clone physical cards for in-person purchases. Possessing or using this data is itself a powerful piece of evidence in a criminal case. The entire process, from the initial search to the final transaction, creates a digital footprint that investigators can follow. The permanent consequences of a criminal conviction far outweigh any potential short-term gain from this high-risk, destructive activity.

Navigating Dark Web Marketplaces

Navigating dark web marketplaces requires a specific set of tools and a significant degree of caution, as these hidden corners of the internet host a vast array of illicit goods. Among the most common offerings are stolen financial details, with many users drawn to the prospect of buying credit cards on the dark web. While forums and vendor shops may seem accessible, every step, from accessing a market like the Ares Market to finalizing a transaction, is fraught with risk. The entire ecosystem is a minefield of scams and law enforcement monitoring, making the act of buying credit cards on the dark web a highly dangerous endeavor with serious legal and financial consequences.

Research and Online Resources

Accessing dark web marketplaces to purchase stolen credit card information is a significant criminal activity with severe consequences. These platforms operate on encrypted networks and are hubs for illicit trade, including the sale of financial data obtained through data breaches, skimming devices, or phishing attacks.

The process of acquiring this data typically involves several steps. First, a user must access the dark web using specialized software that provides a degree of anonymity. Once connected, they would navigate to a marketplace, often found through community forums or directories. After creating an account, they can browse listings that detail the card’s type, issuing bank, country, and sometimes the balance or limit. Payment is almost exclusively made with cryptocurrencies to obscure financial trails.

- Card Dumps: Data copied from a card’s magnetic stripe, used to create counterfeit physical cards.

- CVV2 Data: The card number, expiration date, and CVV code, used for online “card-not-present” transactions.

- Fullz Information: A complete package of personal data, including the card details, along with the cardholder’s name, address, and Social Security Number.

Engaging in these transactions carries immense risk. Beyond the legal repercussions, buyers are frequently defrauded by sellers who provide non-functional or old data. Law enforcement agencies actively monitor these markets, and financial institutions have sophisticated systems to flag fraudulent transactions, making the successful monetization of stolen card information exceedingly difficult and likely to result in prosecution.

Utilizing Onion Link Directories

Navigating dark web marketplaces to purchase stolen credit card information requires specific tools and knowledge. The first step is accessing the dark web itself, which is done using the Tor browser. This software routes your connection through multiple layers of encryption, anonymizing your location and activity. Once on the dark web, users rely on specialized onion link directories to find active and reliable marketplaces where vendors operate.

Engaging in this illegal activity, often referred to as carding, carries extreme risks. Law enforcement agencies actively monitor these marketplaces, and scams are rampant. The process typically involves the following steps after gaining access:

- Locating a reputable marketplace through updated directories and user reviews.

- Creating an account, often requiring a small deposit to prove seriousness.

- Browsing vendor listings that detail the card’s type, country, and balance.

- Selecting a vendor with a strong reputation and a history of successful transactions.

- Funding an escrow account to hold the payment until the product is received.

- Finalizing the purchase and receiving the card’s dumps or card-not-present details.

The entire ecosystem is fraught with danger, from receiving non-functional data to being targeted by authorities. Successful carding is less about technical skill and more about navigating a landscape of deception where every participant is potentially an adversary. The financial and legal consequences for getting involved are severe and long-lasting.

Joining Dark Web Communities

Navigating dark web marketplaces to buy credit cards is a perilous endeavor fraught with significant risks. These platforms, accessible only through specialized software, operate outside the law and are rife with scams. A buyer has no recourse if the received credit card information is invalid or already canceled, making every transaction a gamble. The act of purchasing such data is a serious crime in most jurisdictions, carrying severe legal penalties including imprisonment.

Beyond the immediate financial loss from a scam, the deeper danger lies in the ecosystem you are funding. The sale of stolen credit card information is a primary driver of financial fraud and is intrinsically linked to the crime of identity theft. By participating in this market, you are directly enabling criminals who devastate the financial lives of innocent victims. The consequences for the victim extend far beyond a single fraudulent charge, often requiring years of effort to repair their credit and reputation.

Joining dark web communities centered on this activity does not offer safety but instead increases your exposure. These forums are often monitored by international law enforcement agencies, and participation creates a digital trail that can lead directly to your doorstep. Trust within these communities is an illusion; other members are just as likely to be scammers or investigators as they are to be fellow criminals. Engaging in these spaces only solidifies your involvement in a high-stakes criminal underworld with real-world consequences for both you and the victims whose data you seek to exploit.

Selecting a Reliable Vendor

Selecting a reliable vendor is a critical step when buying credit cards on the dark web, as the anonymous marketplace is fraught with risk. A trustworthy seller not only provides high-quality, valid data but also ensures a degree of operational security for both parties involved. Before committing to any transaction, thorough research into a vendor’s reputation and history on forums is essential. For instance, potential buyers might find relevant discussions and listings on a marketplace like the Abacus Market. This due diligence is the primary defense against fraud when navigating the complexities of buying credit cards on the dark web.

Assessing Vendor Reputation

Selecting a reliable vendor on the dark web when attempting to buy credit cards is a process fraught with extreme risk. The anonymous nature of the ecosystem means that law enforcement operations and outright scams are prevalent. A buyer must approach this with the understanding that every transaction could result in immediate financial loss or, more seriously, lead to severe legal consequences.

Assessing a vendor’s reputation is the single most critical step, as it is the only semblance of a safeguard available. This involves meticulously analyzing their presence on relevant forums and marketplaces over a significant period. Look for a long-standing history of positive feedback, detailed comments from previous buyers confirming the validity of the card data, and a high number of completed transactions. A vendor who has built a strong reputation over many months or years is generally considered less likely to be an exit scam or an undercover operation.

Beyond simple ratings, pay close attention to how the vendor communicates and resolves disputes. Reputable vendors often have clear terms of service and may even offer guarantees or replacements for non-functional cards. They tend to engage professionally with their customer base. Engaging with a vendor who fails these basic checks dramatically increases the risk of receiving worthless data and directly facilitates the criminal enterprise of identity theft, which devastates the lives of victims. The entire endeavor, from search to purchase, carries an unavoidable and high level of danger.

Considering Length of Operation

When navigating illicit marketplaces for financial products, the selection of a vendor is a critical step that carries significant risk. One of the most telling indicators of a vendor’s potential reliability is their length of operation within these volatile spaces. A vendor who has maintained a consistent presence for a substantial period has likely weathered law enforcement actions, market shutdowns, and disputes with buyers. This longevity suggests they have developed a method for operational security and have a track record of delivering on their promises, which is foundational to their vendor reputation.

A long-standing vendor has not survived by accident. Their continued operation implies a history of successful transactions and a degree of customer satisfaction that keeps their business viable. New vendors, while sometimes legitimate, present a much higher gamble; they lack a verifiable history and could easily be an exit scam waiting to happen. The established vendor, conversely, has a reputation to protect, making them more likely to honor deals to maintain their standing and continue their revenue stream.

Therefore, prioritizing vendors with a demonstrable and lengthy operational history is a fundamental risk mitigation strategy. It is a practical filter to separate the potentially credible from the almost certainly unreliable. While no transaction in this realm is without peril, aligning with a vendor who has proven their resilience over time is one of the few concrete measures a buyer can take to slightly tilt the odds away from immediate fraud and loss.

Evaluating Product Quality

Purchasing credit card information on the dark web is a high-risk activity fraught with uncertainty and the potential for significant financial loss. The anonymity of the marketplace means that vendors can disappear without a trace after receiving payment, leaving buyers with worthless data. The first and most critical step is to select a vendor with a proven track record. This involves meticulously researching their history on the forum, reading feedback from previous transactions, and verifying their longevity in the space. A vendor who has been active for a considerable time with consistently positive reviews is generally a safer bet than a new, unproven seller.

Evaluating the quality of the product is equally challenging. Simply trusting a vendor’s description is insufficient. Buyers must rely on community-driven verification. Look for detailed reviews that mention the success rate of the cards, whether they were used for in-person or online transactions, and if the provided information was accurate. A key indicator of a valuable data dump is the inclusion of complete magnetic stripe information. A listing that specifies it contains dumps track 1&2 is often considered more reliable, as this data can be used to clone a physical card, which is a primary goal for many buyers. However, even this is not a guarantee of functionality, as the card may have been reported stolen and canceled by the issuing bank shortly after the sale.

Ultimately, the entire process is a gamble. There is no recourse for a buyer who receives invalid or already-used card information. The most reliable vendors often charge a premium for their products, reflecting the perceived quality and freshness of the data. A seller offering prices that seem too good to be true is almost certainly selling compromised or old information. The entire ecosystem operates on a foundation of distrust, and a successful transaction depends entirely on the buyer’s ability to navigate these opaque reputation systems and make an informed, albeit risky, decision.

Reviewing Customer Support

When navigating the illicit marketplace for buying credit cards, selecting a reliable vendor is the single most critical step to mitigate risk. The anonymity of the dark web provides cover for both legitimate operators and outright scammers, making due diligence non-negotiable. A vendor’s longevity, their presence on multiple marketplaces, and a consistent history of positive feedback are strong initial indicators of reliability. Scrutinize negative reviews with particular care, as they often reveal patterns of selling non-functional data or failing to deliver on promises.

Beyond the initial sale, reviewing the quality of a vendor’s customer support is essential. This is not a typical retail transaction, but the principle of post-purchase service still applies in this criminal context. A vendor who provides responsive and helpful communication before and after a sale is often more trustworthy. This becomes especially important when dealing with data packages known as fullz, which contain comprehensive personal and financial information. If the provided fullz are rejected or lead to a frozen account, a vendor with reliable support may offer a replacement, whereas an unresponsive one will simply disappear with your funds.

Ultimately, the entire process hinges on trust built from the evidence of past transactions. A vendor with a long-standing reputation for selling high-quality, valid data and for standing behind their product with accessible support is the only viable choice. The consequences of failing to properly vet a seller extend beyond financial loss, potentially leading to greater exposure and legal repercussions.

Secure Communication Channels

Engaging in the purchase of credit cards on the dark web is an illicit activity fraught with extreme risk. The entire ecosystem is designed to exploit both the initial victim and the subsequent buyer. The first critical challenge is selecting a vendor who is not an undercover law enforcement officer or a simple scammer. Buyers often rely on feedback systems and forum reviews, but these can be easily fabricated, leaving the purchaser with nothing but a lost cryptocurrency payment.

Once a vendor is selected, establishing a secure communication channel is paramount for criminals seeking to avoid detection. They typically rely on encrypted messaging platforms and email services that prioritize anonymity. All negotiations, from price to the specifics of the stolen data, must be conducted through these channels to shield their identities from both rivals and authorities. The data being sold is often obtained through methods like large-scale data breaches or sophisticated card cloning operations.

The actual data purchased usually consists of the credit card number, expiration date, and the CVV code, a set of information known as “dumps.” The buyer then assumes the immense legal risk of attempting to monetize this information. Law enforcement agencies worldwide actively monitor these marketplaces, and financial institutions have sophisticated algorithms to detect fraudulent transactions, making successful use of the stolen data highly unlikely and leading to severe criminal penalties.

Evaluating Seller Feedback

When navigating the clandestine markets for illicit goods, such as buying credit cards on the dark web, the evaluation of seller feedback becomes a critical line of defense. This digital reputation system is the primary mechanism for gauging a vendor’s reliability and the legitimacy of their offerings. Scrutinizing comments and ratings on a market like Ares Market can reveal patterns of successful transactions or red flags like consistent complaints, directly impacting the safety and success of a transaction involving buying credit cards on the dark web.

Reliability and Trust Assessment

Engaging in the purchase of credit cards on the dark web is an illegal activity fraught with significant risk, and evaluating seller trustworthiness is a perilous and unreliable endeavor. The anonymous nature of the ecosystem means that every interaction is based on a foundation of inherent deception and criminal intent. Buyers have no legal recourse, making the assessment of a seller’s feedback and reputation the only, albeit flimsy, shield against immediate fraud.

When attempting to gauge a seller’s reliability, criminals typically look for specific markers within these illicit marketplaces. The feedback system, while often manipulated, is scrutinized for patterns rather than individual comments.

- Volume and Consistency: A long history of transactions with consistently positive reviews is a primary indicator, though this can be fabricated over time.

- Detailed Feedback: Comments that mention specific product quality, such as the validity of the dumps track 1&2, shipping speed, or communication, are considered more credible than generic praise.

- Verification and Escrow: Trusted sellers often use market escrow services, holding payment until the digital goods are confirmed received. Some may offer a small “test” purchase to prove their dumps track 1&2 are active and high-quality.

Ultimately, any trust assessment in this domain is a gamble. Law enforcement operations frequently create honeypot shops with impeccable feedback to apprehend buyers, and even established sellers can “exit scam,” disappearing with all the funds from unfulfilled orders. The entire process is a high-stakes game where the only certainty is the criminal liability assumed by the participant.

Transaction Satisfaction

Evaluating seller feedback is the single most critical step for anyone navigating the illicit marketplaces of the dark web to purchase credit card information. In an environment devoid of legal recourse, a seller’s reputation, as reflected in past transaction comments and ratings, serves as the primary proxy for trustworthiness. Potential buyers must meticulously analyze this feedback, looking not for generic praise but for specific, verifiable details from previous customers regarding the validity of the card data, the speed of delivery, and the overall professionalism of the exchange.

Transaction satisfaction in this realm hinges entirely on the quality of the purchased data and the security of the interaction. A high volume of positive feedback indicating that cards were “live” and had high balances at the time of use is a strong indicator. Conversely, complaints about dead cards or incorrect PINs are significant red flags. The entire process, from the initial purchase of the data to the subsequent card cloning or unauthorized use, depends on the accuracy of the information provided by the seller. A failed transaction at any point represents a total loss of funds for the buyer, with no possibility of a chargeback or complaint to authorities.

Ultimately, the goal is to minimize risk in an inherently risky endeavor. Scrutinizing feedback for patterns is essential; a seller with a long history of consistent, positive reviews is generally a safer bet than a new vendor offering prices that seem too good to be true. The most satisfactory transactions are those where the received data is accurate, the communication is discreet, and the entire process concludes without drawing any unwanted attention. In the shadowy economy of stolen financial information, a seller’s feedback score is not just a measure of satisfaction, but the closest one can get to a guarantee.

Communication and Support History

Before engaging in any transaction on the dark web, especially for illicit goods like credit card information, a meticulous evaluation of the seller is the single most critical step for mitigating risk. Since no legitimate authority can intervene in case of fraud, the burden of due diligence falls entirely on the buyer. This process involves a deep dive into three interconnected areas: feedback, communication, and support history.

A seller’s reputation is built on their feedback score and, more importantly, the comments left by previous customers. Look for patterns in the reviews that indicate consistency and reliability.

- Examine the volume and longevity of positive feedback. A seller with thousands of transactions over several years is generally more stable than a new account.

- Read negative and neutral reviews carefully to understand specific complaints. Was the card data non-functional, or was the delivery slow? This reveals potential flaws.

- Be wary of feedback that seems generic or fabricated; authentic reviews often contain specific, verifiable details about the transaction and the quality of the data, which is directly linked to the risk of identity theft if the information is faulty or a trap.

Initial communication is a telling indicator of a seller’s professionalism. Prior to purchasing, send a message with a straightforward question. Gauge their response time, clarity, and willingness to provide non-sensitive information. A reputable vendor will typically respond promptly and professionally, while a scammer may ignore you, reply with hostility, or give evasive answers. This interaction tests their operational security and customer service posture before any money is at stake.

Finally, investigate the seller’s history of providing support after a sale. This is often where fraudulent sellers are exposed. Check discussion forums and review sections for mentions of how the vendor handles disputes or reports of invalid data. A trustworthy seller will have a clear policy for replacements or resolutions in case the purchased information is defective. A complete absence of any visible support mechanism or numerous complaints about being ghosted after payment are major red flags. Ultimately, a seller’s willingness to stand behind their product, even in an illegal market, is a powerful signal of their legitimacy.

Payment Methods

The digital underground offers a vast marketplace for illicit financial tools, with buying credit cards on the dark web being a prominent activity for cybercriminals. These markets provide a range of stolen payment methods, from standard bank cards to premium account details, all available for a fraction of their stolen value. The process of buying credit cards on the dark web is often streamlined, with vendors offering customer service and guarantees on their illegal wares. For those navigating these shadowy spaces, resources can be found on sites like the Ares Market, which serves as a hub for such transactions.

Bitcoin and Cryptocurrencies

The dark web hosts numerous illicit marketplaces where stolen credit card information is a primary commodity. These digital stores offer “dumps” of card data, including the cardholder’s name, number, expiration date, and CVV code, often sold in bulk. The entire ecosystem is built upon a foundation of financial fraud, victimizing both the original cardholders and the financial institutions that issued the cards.

Payment for these illegal goods has evolved. While traditional methods still exist, cryptocurrencies, particularly Bitcoin, have become the dominant standard. The perceived anonymity and decentralized nature of these digital currencies make them the preferred medium of exchange for buyers and sellers operating in the shadows of the internet.

Using Bitcoin for such transactions, however, does not guarantee safety. Law enforcement agencies globally are increasingly sophisticated at tracking blockchain transactions. Furthermore, buyers risk being scammed by vendors who take payment and never deliver the promised data. Engaging in these activities is a serious crime with severe legal consequences, and it perpetuates a cycle of financial fraud that damages the global economy.

Escrow Services

The acquisition of payment methods, specifically credit cards, on the dark web is a clandestine process governed by its own set of rules and risks. Transactions in this underground economy rely on a combination of traditional and specialized payment systems to facilitate business between anonymous parties. The inherent lack of trust in these environments makes secure payment handling the cornerstone of any successful, albeit illegal, transaction.

Buyers and sellers utilize a range of payment methods to obscure financial trails. Cryptocurrencies, particularly Bitcoin and Monero, are the dominant standard due to their pseudo-anonymous nature. Other methods may include pre-paid gift cards, wire transfers to mule accounts, or even other digital currencies. The choice often depends on the vendor’s preference and the perceived security of the method.

To mitigate the risk of fraud, where a seller might take payment and not deliver the goods or a buyer might dispute a legitimate transaction, escrow services are commonly employed. A neutral third party holds the buyer’s cryptocurrency until the purchased credit card details are delivered and verified. Only then is the funds released to the seller. This system provides a layer of protection for both sides in an otherwise lawless marketplace.

- Thoroughly investigate vendor reputation by reading feedback and reviews on the marketplace forum.

- Always use the marketplace’s official escrow service for the transaction.

- Never release funds from escrow until you have fully tested and confirmed the validity of the credit card information.

- Be aware that even with escrow, you are dealing with criminals and the possibility of exit scams or law enforcement intervention is high.

Ultimately, while escrow can reduce certain financial risks, it does not eliminate the significant legal dangers or the possibility of receiving worthless data. The entire ecosystem is built on shifting sands, where today’s reliable vendor could be tomorrow’s exit scammer, making constant vigilance and research a necessity for any participant.

Prepaid Cards and Vouchers

The dark web serves as a marketplace for a wide array of illicit financial instruments, with stolen payment card data being a primary commodity. This trade involves the sale of “dumps,” which are the magnetic stripe data from physical cards, and “CVV” information, which includes the card number, expiration date, and security code. Criminals acquire this data through methods like skimming devices, phishing attacks, or large-scale data breaches on corporations.

Beyond traditional credit and debit card numbers, the market also features a significant volume of prepaid cards and gift vouchers. These are attractive to fraudsters because they can be more difficult to trace back to an individual. Stolen prepaid card details are often used for immediate online purchases or to withdraw cash from ATMs before the legitimate owner or issuing company can deactivate them. The anonymity of these instruments makes them a preferred tool for laundering the value obtained from other criminal activities.

The acquisition of this data is almost exclusively conducted using cryptocurrencies, with Bitcoin payment being the dominant method. The pseudo-anonymous nature of these transactions provides a layer of protection for both buyers and sellers, making it challenging for law enforcement to follow the financial trail. This reliance on cryptocurrency is a cornerstone of the entire underground economy, facilitating the exchange of value without the oversight of traditional financial institutions.

Purchasing and using these stolen payment methods carries severe risks. Buyers often receive data that is already expired, canceled, or being monitored by financial institutions. Furthermore, law enforcement agencies actively monitor these marketplaces, and engaging in such transactions can lead to serious criminal charges for fraud, identity theft, and computer crimes. The potential for financial loss and legal consequences far outweighs any perceived benefit from acquiring these illicit goods.

Protective Measures and Precautions

Engaging in the illicit activity of buying credit cards on the dark web is a high-risk endeavor with severe consequences. Beyond the inherent criminality, individuals expose themselves to significant financial and personal dangers, including fraud and identity theft. Any interaction with these markets, such as visiting a site like Abacus Market, should be avoided entirely. The process of buying credit cards on the dark web is fraught with deception, as law enforcement actively monitors these platforms to apprehend participants.

Secure Connections and VPNs

Engaging with illicit platforms to purchase credit cards is a serious criminal offense with severe legal consequences. This activity funds broader criminal enterprises and directly harms innocent individuals through financial fraud. The information presented is for educational purposes only, to understand the risks and reinforce the importance of robust personal cybersecurity.

Before even considering the technological safeguards, the most critical protective measure is understanding the legal and ethical implications. Law enforcement agencies actively monitor darknet markets, and individuals involved in these transactions are subject to prosecution. Furthermore, there is no honor among thieves; sellers on these platforms are criminals who frequently scam buyers, selling invalid or already-canceled card information.

From a technical standpoint, maintaining anonymity and security is a complex challenge fraught with risk. A primary line of defense for any sensitive online activity is the use of a Virtual Private Network (VPN). A reputable VPN encrypts all internet traffic between your device and a remote server, masking your true IP address from your internet service provider and the websites you visit. This prevents eavesdroppers on your local network from seeing your online activities.

However, a VPN alone is insufficient and can create a false sense of security. It is merely one layer of a broader security posture. The provider of the VPN service can still see your traffic and, depending on their jurisdiction and logging policies, may be compelled to hand over data to authorities. For maximum security, this must be combined with the use of the Tor Browser, which is specifically designed to anonymize web traffic by routing it through multiple volunteer-operated servers around the world.

Beyond connection security, operational security is paramount. This includes using operating systems designed for anonymity, creating unique and complex credentials for every service, and employing end-to-end encrypted communication tools. It is also vital to disable JavaScript and other plugins that can be exploited to reveal your identity. Your own behavior is often the weakest link; even with advanced tools, a single mistake can compromise your entire operation. Ultimately, the only truly effective protective measure is to avoid engaging with these illicit platforms entirely.

Encrypted Communication

Engaging in the illicit activity of purchasing credit cards on the dark web is a serious crime with severe legal consequences. This article describes the security environment for informational purposes only, emphasizing the significant risks and illegal nature of such actions. Individuals involved in these markets operate in a constant state of paranoia, aware that law enforcement agencies are actively monitoring these spaces. The anonymity provided by the dark web is a double-edged sword, as it also shelters scammers and malicious actors who have no intention of delivering the promised goods.

Before any transaction is even considered, extensive research into the seller is paramount. The single most critical factor for a potential buyer, beyond price or product listing, is the vendor reputation. This is built over time through feedback and reviews on the marketplace forums. A vendor with a long history of positive feedback is generally considered more reliable, though this is never a guarantee. New or poorly reviewed vendors present an enormous risk of being an exit scam, where they take payments and then vanish without delivering anything.

Encrypted communication is non-negotiable for all parties involved in these illegal exchanges. All discussions, from initial contact to the finalization of a deal, must occur through secure, end-to-end encrypted channels. The use of standard email or unencrypted messaging services is considered reckless, as these communications can be easily intercepted and used as evidence. The preferred method is often PGP encryption, where each party uses a public key to encrypt messages that can only be decrypted by the corresponding private key. This ensures that even if a marketplace is compromised, the private conversation between a buyer and seller remains confidential.

Financial transactions themselves are conducted using cryptocurrencies, primarily for their pseudo-anonymous nature. However, simply using a cryptocurrency like Bitcoin is not sufficient, as its blockchain is public and traceable. Sophisticated actors will use privacy-focused cryptocurrencies or utilize mixing services to obfuscate the trail of funds. The entire process, from browsing and communicating to transacting, must be done through the Tor network to conceal the user’s IP address and physical location. Despite these extensive protective measures, there is no such thing as perfect security, and participants are always one mistake away from identification and prosecution.

Operational Security (OpSec)

Engaging in the purchase of credit cards on the dark web is an illegal activity with severe legal consequences. This text describes the associated risks and security practices from an analytical standpoint only. Individuals involved in this trade, often referred to as carding, operate in a high-stakes environment where law enforcement monitoring is constant and other participants are often hostile.

Protective measures for these actors begin with robust digital hygiene. This includes using a secure, non-Windows operating system run from a live USB to leave no trace on the host machine. All activities must be routed through the Tor network, and a reputable VPN service should be chained before the Tor browser for an added layer of obscurity. Disk encryption is mandatory for any persistent storage. Communications must be secured with end-to-end encrypted messaging platforms, and all metadata, such as language settings and timezone, must be meticulously spoofed to prevent de-anonymization.

Operational Security, or OpSec, is the continuous process of managing digital footprints. This involves creating and maintaining compartmentalized identities, or personas, for all activities. Each persona must have unique credentials, email accounts, and cryptocurrency wallets, with absolutely no crossover between these operational identities and one’s real-life identity. All financial transactions utilize cryptocurrencies like Monero or Bitcoin, but only after being laundered through a series of intermediary wallets or a mixing service to break the transaction trail. Trust is a vulnerability; even with established vendors, the principle of assuming every interaction is compromised must be upheld.

Managing Digital Footprint

Engaging in the purchase of credit cards on the dark web is an illegal activity with severe legal consequences, including felony charges and substantial prison sentences. Beyond the legal ramifications, it exposes individuals to significant personal risk, as they are interacting with sophisticated criminal networks who are just as likely to defraud the buyer as they are to provide a legitimate service. The entire ecosystem is designed for anonymity and deception, making any transaction a high-stakes gamble.

For the general public, the primary protective measure is to safeguard personal financial information proactively. This involves using strong, unique passwords for all financial accounts and enabling multi-factor authentication wherever it is offered. Regularly monitoring bank and credit card statements for any unauthorized transactions is crucial, as is signing up for transaction alerts from your financial institution. Furthermore, individuals should exercise extreme caution with their personal information online, being wary of phishing attempts via email or fraudulent websites designed to steal login credentials.

Managing your digital footprint is a critical component of this protection. A digital footprint is the trail of data you leave behind while using the internet, and a large, poorly managed footprint increases your vulnerability. This includes being mindful of the information shared on social media platforms, such as birthdates, addresses, or even details about a new card, which can be pieced together by malicious actors. Limiting the amount of personal data available online makes it harder for criminals to build a complete profile for identity theft or targeted attacks.

For those who might be tempted to explore these illicit markets out of curiosity or financial desperation, the risks cannot be overstated. The concept of vendor reputation on these platforms is a dangerous illusion. While some forums feature rating systems, these can be easily manipulated through fake reviews or coordinated efforts by the vendors themselves. There is no consumer protection, no recourse for a fraudulent sale, and every interaction confirms your involvement in a criminal enterprise to the platform operators and law enforcement. The only safe and prudent course of action is to completely avoid these dark web marketplaces and report any discovered instances of them to the appropriate authorities.

Limiting Financial Exposure

Engaging in the purchase of credit cards from the dark web is an illegal activity with severe legal consequences. This action constitutes fraud and is aggressively prosecuted by law enforcement agencies worldwide. Beyond the legal ramifications, buyers expose themselves to significant personal risk, including scams where no valid cards are delivered, malware infections, and targeting by other criminals. The fundamental precaution is to avoid this activity entirely.

For individuals concerned about their financial security, legitimate protective measures are essential. Regularly monitoring bank and credit card statements for any unauthorized transactions is a critical first step. Enabling instant transaction alerts through your financial institution provides real-time notification of activity. Furthermore, using strong, unique passwords for all financial accounts and enabling multi-factor authentication adds a powerful layer of security against account takeover attempts.

Limiting financial exposure is a cornerstone of sound financial management. This involves using credit cards with lower spending limits for daily transactions, as they inherently cap potential liability. Many banks allow you to set custom transaction limits or even temporarily lock a card via their mobile app. For any online purchase, especially on less familiar sites, consider using a virtual credit card number, which masks your actual account details. A transaction completed with a Bitcoin payment is irreversible, which is why criminals favor it, but for a consumer, this permanence is a significant risk when dealing with an unverified seller.

Ultimately, the most effective way to limit financial exposure from dark web threats is to never engage with these markets. The promise of cheap goods or financial gain is a trap that leads to legal trouble, financial loss, and compromised personal security. Vigilance and robust, legitimate security practices are the only true protection.

Safe Access Procedures

Navigating the digital underground requires stringent Safe Access Procedures to mitigate significant risks. For individuals considering the illicit activity of buying credit cards on the dark web, understanding operational security is paramount. This involves using specialized software, maintaining anonymity, and verifying sources through trusted community hubs like the Abacus Market. The dangers associated with buying credit cards on the dark web extend beyond financial loss to include severe legal consequences, making robust security protocols not just a recommendation, but a necessity.

Using the Tor Browser

Engaging in the purchase of credit cards on the dark web is an illegal activity with severe legal consequences. This article describes the security procedures used by individuals involved in such markets for educational purposes only, to highlight the risks and methods of cybercrime. Understanding these practices is crucial for developing effective cybersecurity defenses.

Before accessing any dark web resource, one must first download and verify the official Tor Browser from its legitimate source. This browser is fundamental for anonymizing network traffic by routing it through a global volunteer overlay network. It is critical to ensure the browser is up-to-date before each session to protect against known vulnerabilities that could de-anonymize a user.

A core component of safe access involves operational security. Users often operate within a dedicated, clean virtual machine that is isolated from their host operating system. This VM should have no personal data, and all its network connections must be forced through the Tor network. Disabling JavaScript within the Tor Browser is a common, though not always practical, precaution to prevent exploit-driven attacks.

Once on a marketplace, the process of carding involves significant risk beyond legality. Vendors and buyers operate with a high degree of paranoia. All communications should be encrypted, typically using PGP, even within the supposedly private messaging systems of the market itself. Trust is a rare commodity, and reputation systems are often manipulated.

Ultimately, the entire ecosystem is fraught with danger. Law enforcement agencies actively monitor these spaces, and participants are frequently targets of scams by other criminals. The promise of financial gain is overshadowed by the high probability of financial loss, arrest, and prosecution. There is no safe or reliable way to participate in these illegal activities.

Disabling JavaScript and Plugins

Engaging in the illicit activity of purchasing credit cards on the dark web carries severe legal consequences and significant personal risk. Individuals involved in such actions often employ specific safe access procedures in a misguided attempt to shield their identity. This typically involves the use of specialized software to route internet traffic through multiple layers of encryption, providing a degree of anonymity.

A common step in this risky process is the disabling of JavaScript and browser plugins within the specialized browser used for access. The rationale behind this is to prevent potential security vulnerabilities that could be exploited to reveal a user’s true IP address or install tracking malware. By deactivating these features, the user aims to create a more sterile and secure browsing environment, reducing the number of potential attack vectors that could compromise their operation.

However, it is critical to understand that these measures are far from foolproof. Law enforcement agencies actively monitor these marketplaces and employ advanced techniques to de-anonymize users. Furthermore, the dark web is rife with scams; sellers often provide stolen or invalid card information, and other users may attempt to exploit anyone they perceive as a target. The act of disabling JavaScript itself can make a user’s browser fingerprint more unique and thus easier to track across different sites.

Employing Firewalls and Antivirus

Attempting to purchase credit cards on the dark web is an illegal activity with severe consequences. Beyond the legal ramifications, individuals who engage in this behavior expose themselves to significant personal risk. The very markets and vendors offering these stolen financial instruments are operated by criminals who have no incentive to act honorably. A buyer is just as likely to become a victim, receiving non-functional data or, worse, having their own payment and personal information stolen for further exploitation.

For legitimate organizations, protecting against the misuse of stolen card data requires robust safe access procedures. This involves implementing strict identity and access management (IAM) policies to ensure that only authorized personnel can access sensitive financial systems. Multi-factor authentication, the principle of least privilege, and detailed access logs are fundamental components. These measures create a defensive barrier, making it exponentially more difficult for unauthorized users, whether external hackers or malicious insiders, to leverage stolen data for financial fraud within the corporate network.

A critical technological layer in this defense is the proper employment of firewalls and antivirus software. A correctly configured firewall acts as a gatekeeper, monitoring and controlling all incoming and outgoing network traffic based on an established set of security rules. It can block communication attempts from known malicious servers, including those used by criminals on the dark web. Meanwhile, comprehensive antivirus and anti-malware solutions are essential for endpoint protection. They work to detect, quarantine, and eliminate malicious software that might be designed to steal card information directly from a user’s device or to create a backdoor for an attacker.

Ultimately, the combination of stringent administrative controls and powerful technical security tools forms a cohesive defense strategy. This layered approach is vital for any entity handling payment card information, as it directly counters the threats posed by the underground trade of stolen data. The focus must remain on prevention and security, not on engaging with the criminal ecosystems that fuel these attacks.

Password Hygiene

Attempting to purchase credit cards on the dark web is an illegal activity fraught with extreme risk. Beyond the severe legal consequences, individuals expose themselves to a high probability of being defrauded or having their own information compromised. For anyone navigating these spaces for other reasons, understanding safe access procedures and password hygiene is critical for personal security.

Accessing any restricted network requires a disciplined approach. The use of specialized software is non-negotiable, and it must be kept updated to the latest version to patch known vulnerabilities. All network connections should be routed through the Tor network to obfuscate your IP address and location. Furthermore, your operating system’s firewall should be enabled and configured to block all unnecessary inbound and outbound connections, creating a vital barrier against unauthorized access.

- Use a dedicated, hardened operating system designed for security and privacy.

- Disable scripts and plugins within your browser to prevent drive-by exploits.

- Verify the authenticity of any dark web links from multiple independent sources.

- Never use the same username or email address across different dark web services.

Once inside these environments, password hygiene becomes your primary defense. Criminals operating on these platforms are themselves targets for hackers and law enforcement, meaning any database of user accounts is a high-value target. Assume that every marketplace forum you register for will eventually be seized or scammed. Therefore, you must create a unique, complex password for every single site you visit. A strong password manager is essential for generating and storing these credentials securely.

- Generate passwords that are at least 16 characters long, using a random mix of letters, numbers, and symbols.

- Enable two-factor authentication (2FA) on every service that offers it, preferably using an authenticator app.

- Never reuse a password from your normal internet activity on any dark web site.

- Be highly suspicious of any site that does not require robust security practices from its users.

Financial transactions in these illicit spaces are deliberately opaque. Sellers demand payment in cryptocurrencies to maintain anonymity, and a Bitcoin payment or other cryptocurrency transfer is typically required upfront. This creates a situation of zero buyer protection; once the funds are sent, they are gone. There is no bank or credit card company to reverse the charge if the seller never delivers the promised goods, which is a common exit scam. The combination of strong access procedures and impeccable password hygiene is the only way to mitigate some of the operational risks, though it does nothing to lessen the significant legal peril involved.

The Purchasing Process

The purchasing process on the dark web involves navigating a series of deliberate steps to acquire illicit goods, with buying credit cards on the dark web being a prominent example. This journey typically begins with accessing specialized marketplaces and forums, where vendors and buyers connect under a veil of anonymity. A crucial phase involves vetting sellers and their offerings to mitigate the high risk of fraud, a common pitfall when buying credit cards on the dark web. For those seeking financial tools, one might visit a resource like the financial hub. The final steps encompass a secure transaction, often using cryptocurrencies, and the subsequent receipt of the digital goods, completing the clandestine cycle.

Accessing Reputable Marketplaces

The process of purchasing credit cards on the dark web follows a structured, albeit illicit, procurement cycle similar to conventional e-commerce. A buyer must first access specialized marketplaces using anonymizing software. These platforms operate as digital bazaars where vendors list stolen financial data, often with customer reviews and ratings to establish a semblance of credibility. The entire operation is a criminal enterprise designed to facilitate financial fraud.

Accessing reputable marketplaces is a critical and risky step. The term “reputable” here is relative, referring to platforms known for consistently delivering the stolen data as advertised and having a lower likelihood of being an exit scam. Potential buyers often rely on community forums and feedback systems to vet these markets before engaging in any transactions.

- Acquire and configure the necessary anonymity tools.

- Navigate to a trusted dark web forum or directory.

- Research and select a marketplace based on user reviews and longevity.

- Create an account, often requiring a referral or invitation.

- Browse vendor listings, paying close attention to the card’s issuing bank, type, and balance.

- Fund an escrow account using cryptocurrency.

- Finalize the purchase and receive the card details.

The purchased data typically includes the card number, expiration date, CVV code, and sometimes the cardholder’s name and address. Possessing this information allows criminals to make unauthorized online purchases or create cloned physical cards. This act is a direct form of financial identity theft, causing significant monetary loss and credit damage to the victim whose information was compromised. The entire ecosystem thrives on the exploitation of stolen personal and financial data.

Selecting Credit Card Details

The process of purchasing credit card details on dark web markets follows a surprisingly structured, albeit illicit, commercial flow. A buyer begins by accessing a specialized marketplace and navigating to the financial data section. Here, they are presented with numerous listings from different vendors, each offering dumps, CVV2 numbers, or fullz (complete information packages). The sheer volume of options makes the selection phase critical to the entire operation’s success.

Selecting the specific credit card details involves careful scrutiny of the listing itself. Buyers meticulously review the provided information, which often includes the card’s brand, type, issuing bank, and country of origin. The price is heavily influenced by the perceived validity and freshness of the data, the credit limit, and whether the card is a Visa or Mastercard. Crucially, a buyer’s decision is almost entirely dependent on vendor reputation, which is built from historical transaction feedback and ratings left by previous customers. A vendor with a long and positive track record for selling live and high-balance cards can command significantly higher prices.

Once a vendor and listing are chosen, the buyer proceeds to checkout. This typically involves transferring cryptocurrency into the marketplace’s escrow system, which holds the funds until the product is delivered and verified. After payment is secured, the vendor releases the credit card details—the card number, expiration date, CVV code, and sometimes the cardholder’s name and address. The buyer then quickly tests or uses the information before the card is reported stolen. This entire process underscores a parasitic digital economy where trust is commodified and financial theft is systematized.

Initiating Contact and Negotiating

The process of acquiring credit card information on the dark web is a methodical and illicit activity that mirrors legitimate e-commerce in its structure. It begins with a buyer identifying a marketplace or a specialized forum where such data is traded. These platforms operate with a focus on anonymity, requiring the use of specific browsers and often cryptocurrency for any transaction. The initial step involves extensive research to find a vendor with a reputation for selling “fresh” and valid data, as the entire endeavor hinges on the quality of the stolen information.

Initiating contact with a seller is a cautious dance built on perceived trust and verified reputation. Buyers rarely communicate directly at first; instead, they rely on marketplace feedback systems and forum reviews. A vendor’s long-standing presence and positive comments from previous buyers are the primary indicators of reliability. Once a seller is selected, a buyer might use the marketplace’s encrypted messaging system to ask specific questions about the card’s origin, its recent activity, or the inclusion of other personal details, always being wary of law enforcement operatives or scammers.

The negotiation phase is where the final terms of the illegal exchange are settled. Price is often determined by the card’s type, the issuing bank, the cardholder’s geographic location, and the available balance. Sellers on these CVV shops typically have fixed rates for different tiers of data, but bulk purchases can sometimes be negotiated. The buyer must send the cryptocurrency payment, often to an escrow service held by the marketplace, before the seller releases the data. This entire process is a high-stakes gamble, with the constant risk of financial loss, arrest, or receiving completely worthless information.

Making Payment and Receiving Data